Neil, a successful businessman, was fascinated by an amazing launch video of a newly launched electric sports car. The machine could rev up from 0 to 100 km/hr in a matter of few seconds. His friend Nick sensed Neil’s desire and advised him “Neil, why don’t you immediately go ahead and place an order for this dream machine. After all, you will be buying an ‘asset’.”

Nick’s statement reflects the commonly held perception of assets. Hence we need a quick primer on accountancy first. Basics study of Accountancy include concepts of an asset, liability, income, expense, etc. An accountant’s definition of an asset is any resource that is owned or controlled by a company or individuals and which can provide a benefit in current and future periods. A liability is something a person or company owes, usually a sum of money.

Some of the common assets according to his definition are:

- Cash and Bank balances

- Investments in shares, bonds or any other security

- Inventory of raw materials or finished goods

- Office equipment

- Machinery

- Real estate like Apartment or Office premises

- Vehicles like cars, trucks

- Patents or Trademarks for products or services

The common thread running across all assets as defined by accountancy include:

- They last for more than one year

- They provide certain benefits or value to its owner or possessor

However, from the lens of personal finance, not all assets are created equal. Some are good to accumulate, while some are not. Some assets generate income for its owner, while some just satisfy the possessor’s needs or wants.

Consumption Assets: These are assets which just satisfy the needs or wants of its possessor. They do not generate capital. On the contrary, they might need some recurring expenditure for repairs or maintenance on an ongoing basis. Consumption assets are like liabilities, which entail a regular net outflow.

Some of the examples of Consumption Assets are:

- Our house property in which we live: The residential property in which we live is a Consumption Asset. It satisfies our basic need of shelter. However, it entails regular expenses for maintenance and repairs.

- Car for self-use: Our car helps us with our daily commute. However, it also entails regular expense in the form of fuel, insurance, repairs and maintenance.

Productive Assets: These are Assets which generate Income for its owner on a regular basis. While they may also need repairs or maintenance, they generate money for its owner on a net basis. These are good to own assets and ones which we should aim to accumulate over our lifetime to achieve our goals of financial freedom.

Some of the examples of Productive Assets are:

- Our house property given on rent: The residential property given on rent generates Rental Income, which is in excess of the regular expenses for maintenance and repairs. The property also appreciates in value and can generate Capital Gains Income whenever it is sold in the future.

- Owned Truck given on contract: Our owned Truck given to a logistics company on contract, generates freight income. While it entails regular expense in the form of fuel, insurance, repairs and maintenance, the freight income is significantly higher than such expenses.

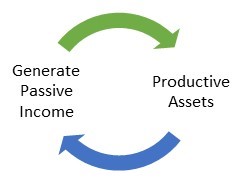

Some of the popular productive assets are investment in shares and bonds, real estate for rent like office premises, investment in own business ventures, etc. Income from productive assets is also called passive income, as an individual does not need to actively work to earn this income. His assets ‘work’ for him to generate this income.

When we aspire for financial freedom, we should endeavor to accumulate productive assets. These assets, in turn generate passive income, which can be utilized to accumulate more productive assets. This activates the virtuous cycle of passive income.